The New AgFunderNews AgriFoodTech Report is Here

It’s here! Yes, folks, last week was World Agri-Tech in San Francisco, and so once again that means that the team at AgFunderNews released their annual report Global AgriFoodTech Investment Report 2026, which goes in-depth (as always!) into the funding highlights and analysis of why things changed in 2025 and are likely to continue changing in 2026. I have had the chance to read the report for the first time this week. I will give it a couple more reads in the next few weeks, and I often like to compare the content and context to prior years to see where there are some lessons to be learned across multiple years that you don’t always get from a single year analysis. The AgFunderNews is one of the key pieces of analysis for AgriFoodTech. It’s the AgriFoodTech version of Mary Meeker’s Internet Report, and it’s absolutely must-see TV (or must-read print!).

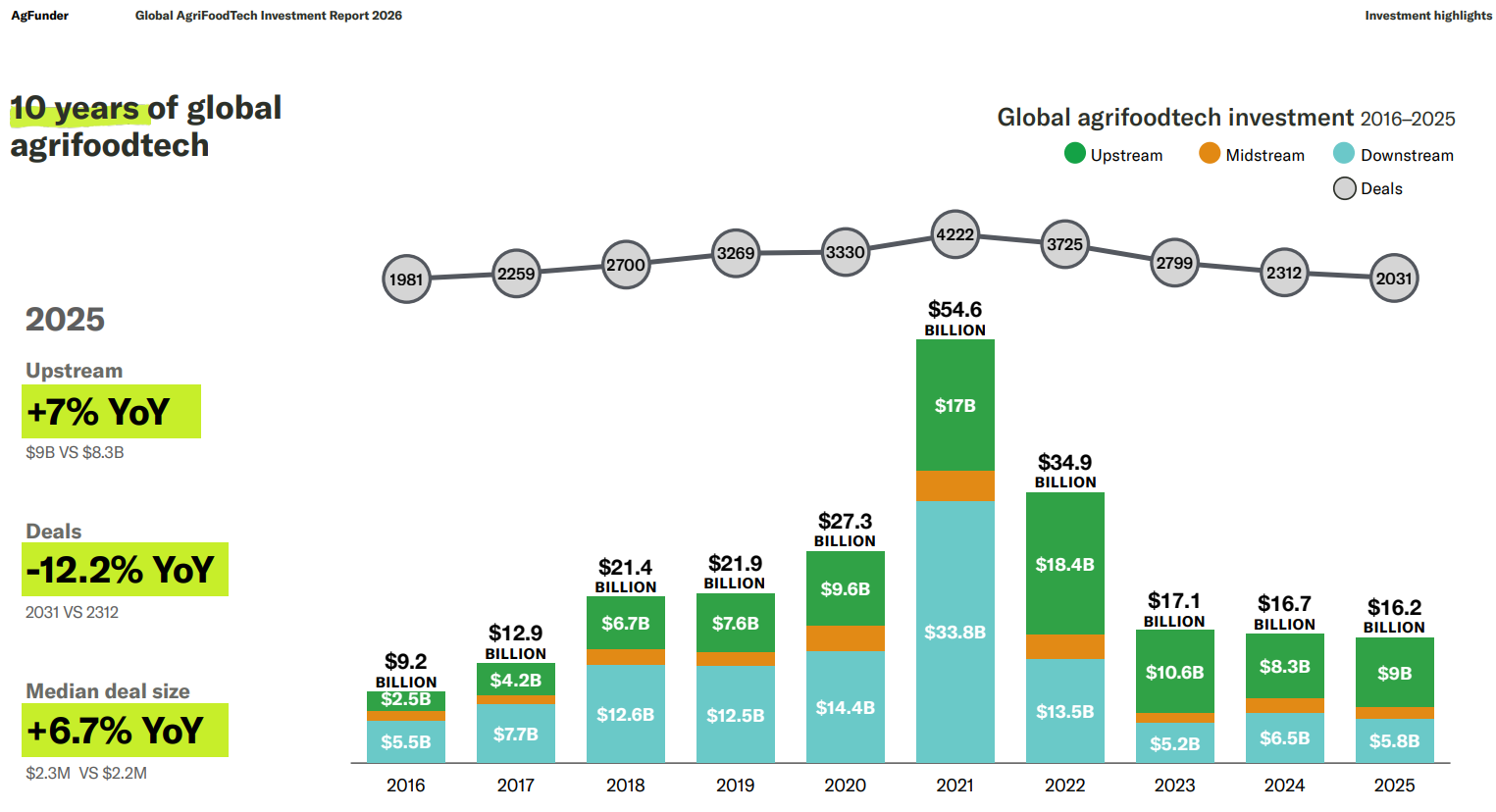

For today’s article, I wanted to highlight what I believe is the most significant graphic. It’s the classic 10 years of Global Agrifoodtech that now goes from 2016-2025. That graphic is here, and there’s a lot to discuss.

Let’s get right to the most important number: $16.2 billion. That is the total amount of AgriFoodTech VC for 2025. This number tells us a lot about 2025. First, it tells us that while the first half of 2025 was horrendously low in investment capital at $5.1 billion (always worth reminding everyone that the annual number for 2021 was $53B, so $26.5 would be a half year estimate for comparison shopping purposes. Clearly that’s a much different baseline than the $5.1B we saw in the first half of last year), the second half of 2025 got significantly better at $11.1, thus the $16.2B total.

While it is true that in many tech segments the second half (or back half) of the year can be heavier than the front, the first half of 2025 was troubling because coming off the drop from $54.6B in 2021 to $34.9B in 2022 to $17.1B in 2023 to $16.7B in 2024, many of us were of the belief that the small drop from 2023 to 2024 suggested that we had reached the bottom of the trough and things would stabilize. After all, $54.6B to $16.7B represents a 69% drop in three short years, and many of us were hoping to find the bottom sooner than later. But we found no support at all for the alleged new baseline in the 1H2025 number ($5.1B). In fact, you can argue that this is why many were hesitant to put much confidence in a second half resurgence. Things looked pretty grim in July and August of 2025, and $10B seemed like a very real possibility for the 2025 total. So many of us described the forecast for 2025 after the first-half number as $10-12B (to capture a little upside) or $8-12B (to put the $10B as the midpoint of a reasonably large range).

Even worse, to many of us who watch the space closely, as we talked to startups and investors and watched transaction announcements and activity, it did not seem like the second half of 2025 was likely to generate much beyond the first half. On this count, I am very happy to be proven wrong. On all fronts, the $16.2B total for 2025 is actually a big win. Being able to use a $15-17B or $16-18B range as your total AgriFoodTech VC funding amount for 2025 (depending on how conservative you want to be) is a lot better than $8-12B or even $10-12B.

The other point to remember for AgriFoodTech VC at a high level is that we’ve gotten rid of a lot of capital from two of the dumpster fires of 2021 (vertical farming/CEA and alternative proteins – 42% of that $54B number and none of it ended well) and now (for the moment) stabilized in the $15-17B range. Every dollar that those two categories have been reduced by de-risks the AgriFoodTech VC segment as a whole and thankfully there have been billions of dollars in reductions. I see much less risk in vertical farming today than I did even two years ago.

I still have some concerns about the alt-protein category, but that’s a topic for another day. For now, it’s worth noting that of those two dumpster fires, alt-protein is by far the one with the most smoke still lingering around and therefore the higher risk factor of the two, but it’s a lot less risk than just a few short years ago.

So, we have a much healthier baseline for AgriFoodTech VC than we did just six months ago ($16.2B v $10B), and we have de-risked two of the riskiest segments and 42% of the whole category from five years ago. Time will tell if we can maintain the new range of $15-17B (to be conservative). Our first two data points will be the Q1 and H1 checkpoints at the end of Q1 and Q2 this year.

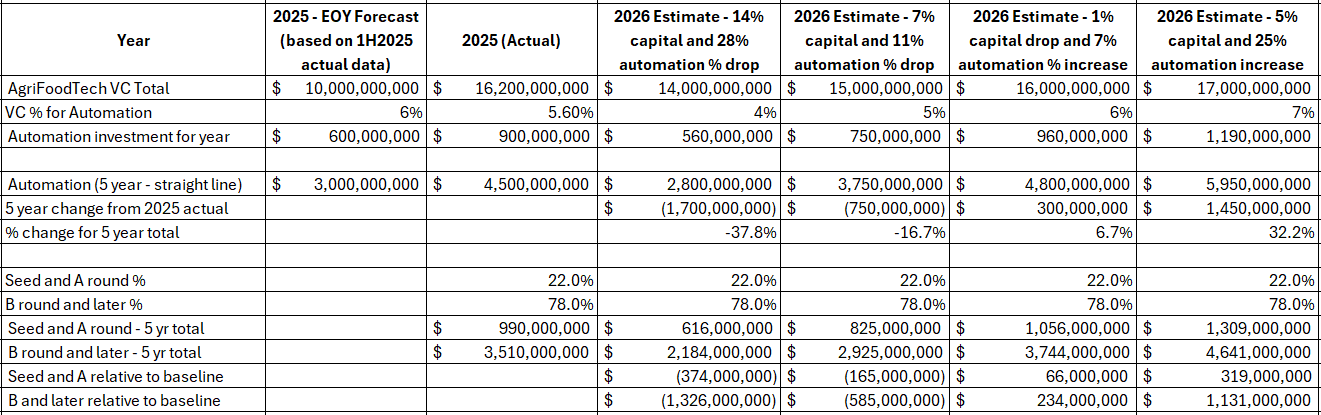

With the significance of the overall total discussed, let’s take a look at the main category related to California grower economic challenges: labor. Second, when we dive into the automation segment specifically, recall that earlier I posted that automation is averaging 4-7% of total AgriFoodTech investing and trending up (currently at about 6%). If you take 6% of $10B (the estimate I was using for 2025 until actual numbers landed), you get $600M as the annual investment in automation. That was the number I’ve been using, and obviously if you baseline five years of investment and don’t see much cause for big increases (because growth in AgriFoodTech VC is unlikely to happen until exits, either IPOs or M&A, picks up in a meaningful way), you can straight-line the numbers to $50B in AgriFoodTech VC over five years and $3B (6%) as the target for automation/robotics. That was the number I’ve been using as a five-year automation investment target for a few months.

Now that the real number has landed at $16.2B and the real number (which will be in a graphic further down) for automation for 2025 was $900 million, you see two things. We are well above the $10B target (as above – 62% above) I’ve been using for AgriFoodTech and (as importantly, particularly for robotics startups) well above the $600M target for automation (in fact we are 50% above it). As importantly, if you take $900M as the automation spend out of $16.2B, you see that last year automation was at 5.6% of total. This provides support for the 6% baseline I used for the five-year projection.

And here we get to the fun with spreadsheets portion of the article, and who doesn’t like to see some fun with spreadsheets in an AgTech article? I went through a couple of modeling exercises and played them all the way out. In the spreadsheet below, you can see that I took the old 2025 forecast (when all we had was first half of 2025 data) and compared it to actual in the first two columns, then ran the numbers out straight-line as a baseline for a five-year projected total. Then I took four different scenarios that used different amounts of overall AgriFoodTech VC funding and the percentage of that funding that was in the automation category. The four scenarios I used for total AgriFoodTech VC were $14B, $15B, $16B, and $17B. The four scenarios I used for automation were 4%, 5%, 6%, and 7%. You can see the details here.

Based on the actual data we now have from 2025, I believe the most likely baseline (i.e. which one of the four is most likely to be closest to both numbers) is the third column, which uses $16B and 6%. Recall that the actual numbers for 2025 turned out to be $16.2B and 5.6%. I think the $16B number represents a fair annual baseline because a lot of the poorly performing segment capital has gone away and is not likely to suffer an additional large drop. I think the 6% number represents a fair automation percentage baseline because automation is the category that is most closely aligned to solving specialty crop grower’s primary challenge – labor and the cost and availability of it. I think it will continue to grab share from categories that are less clear about the grower problems they are solving or even less clear about the grower economics they need to reach to become a solution growers purchase. You can see the range of outcomes in the four models when you focus on the five-year forecast numbers for each of the models. There is a range of $1.7B lower in the first model to $1.5B higher in the last model.

Recall that I posted a couple weeks back on the shifting investment landscape as we went from 78% funding for seed to A round investments 10 years ago and 22% funding for B round and later to an exact flip today. Today, we have 78% going to B round and later and 22% going to seed to A round. There are multiple reasons for this, the primary one being that a lot of VCs are choosing portfolio protection over new investments and choosing to double down on existing investments with new rounds at a much higher rate (78%), which leaves much less capital for early stage first time investments (22%).

I outlined in that piece that we now have a $1B shortfall in funding needed for a healthy automation innovation funnel because of this shift. The reason to continue watching the capital shift by stage is to provide further support and more data for the argument. One of the more likely sources of capital that can help close the $1B shortfall is federal or state funding from DC and Sacramento based on an economic development thesis because of all the jobs agriculture and AgTech create and support in rural economies. The economic development skews heavily toward rural job creation and minority job creation and job up-skilling.

We will continue watching the overall AgriFoodTech VC number, the automation number, and the shift-mix from seed to A to B and later with an eye on helping both DC and Sacramento remember that ag and AgTech work closely together to support ag GDP and jobs, AgTech GDP and jobs – particularly in automation. The ag and AgTech then create additional opportunities for things like automation integration (integrating the robots into farming operations after they are sold and need to be supported) and data/analytics solutions, as well as circular economy GDP and jobs created from the opportunity that hundreds of thousands of acres of permanent crops (trees and vines) and 6,000 ag and food processing facilities creates around reuse and recycle of both of those product sets into things like new ingredients and new jobs and GDP.

For today, the key points from the most important graphic of the AgFunderNews annual report are these:

1) $16.2B is a great total for 2025 AgriFoodTech total VC investments given the risk factors and concerns many of us had just six months ago. Ideally, this total represents a new baseline range that AgriFoodTech VC can maintain. We will know as the quarterly actual numbers land each quarter of 2026.

2) $900M is a solid total for automation and keeps its percentage of AgriFoodTech VC spending at 5.6%. I expect automation to continue to gain share of investment because it’s solving real problems related to labor availability and cost.

3) The four scenarios I modeled with AgriFoodTech annual investment at $14B, $15B, $16B, and $17B, and the % on automation at 4%, 5%, 6%, and 7% create a wide range of 5-year automation investment totals (from $1.7B below baseline to $1.5B above baseline). These scenarios are important because they allow us to adjust in real time as new data arrives and as we make fundraising requests and measure the economic development impact of capital from all sources.

4) At this point, the most likely baseline scenario for 2026-2030 for automation VC investment is $4.8B, which models AgriFoodTech VC at $16B a year (up from $10B a year previously) and models automation investment at $960M a year (up from $600M a year previously). In the most likely scenario, the model suggests $1.1B for seed to A round investments over five years and $3.7B for B round and later investments over five years. All of these numbers are well above the former model, which is good news for startup founders. Now we watch and see how 2026 plays out and if we need to make additional model adjustments.

{kind=link}

{kind=link}

More about Next Gen AG Workers

Western Growers and the California Women for Agriculture Coachella Valley Chapter Host Student Ag Careers Tour

WG’s Walt Duflock Joins Farm Automation Panel at World Agri-Tech Summit in San Francisco

FARMX: Revolutionizing Agriculture

Walt Duflock Talks the Future of California Ag with The Modern Acre Podcast